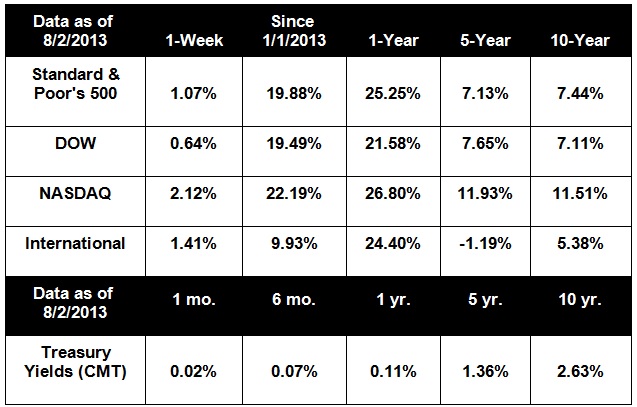

Markets closed out another positive week, driven upward by a better-than-expected GDP report and a reminder that the Fed won't be pulling the plug on bond purchases this month. Nervousness ahead of a Fed policy meeting and the monthly jobs report contributed to volatility, but the rally pushed the S&P 500 to a new historic high.[1]

The big economic news last week was the July jobs report and a first look at second quarter GDP. The initial GDP report shows that the economy grew 1.7% in Q2, handily beating economists' estimates of 1-1.1% growth. A buildup of business inventories was enough to offset the effects of sequestration, thus accounting for the surprising jump. On the whole, we view the report as a positive, showing that the economic recovery is gaining momentum. Although it's too soon to make any accurate predictions about future growth, some economists expect expansion to accelerate to 2.3% in Q3 and 2.6% in Q4, for a strong finish to the year.[2]

The jobs report was a mixed bag; hiring slowed in July, with the addition of only 162,000 new jobs, the smallest gain in four months. However, July employment numbers are notoriously unreliable, due to seasonal factors like factory closings. All things considered, it is worth noting that the month's job gains were enough to drive the headline unemployment rate down to 7.4%. These mixed signals could make the Fed cautious about tapering bond purchases too soon, and some analysts now believe it could be October or December before we see tapering begin.[3]

The Federal Reserve FOMC met last week but announced no policy changes, meaning that current quantitative easing programs will continue for the near future. The meeting announcement (which provides a brief summary of the meeting) offered little additional guidance about future Fed moves.[4] In a separate interview, a top Fed official stated that the recent drop in the unemployment rate took the country one step closer to the 7% unemployment threshold set by Fed chairman Ben Bernanke as the point around which the central bank would likely end its QE bond purchases.[5]

With earnings season wrapping up, a light calendar of economic data, and a few solid weeks of growth behind us, it's possible that we may see a short-term decline as traders take profits and wait for news from the Fed. In any case, we hope you enjoy your week, and that you don't spend too much time focusing on every Fed announcement and piece of economic news. In the words of Edmund Burke, "If we command our wealth, we shall be rich and free; if our wealth commands us, we are poor indeed."

ECONOMIC CALENDAR:

Monday: ISM Non-Mfg. Index

Tuesday: International Trade

Wednesday: EIA Petroleum Status Report

Thursday: Jobless Claims

Notes: All index returns exclude reinvested dividends, and the 5-year and 10-year returns are annualized. Sources: Yahoo! Finance and Treasury.gov. International performance is represented by the MSCI EAFE Index. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly.

The Standard & Poor's 500 (S&P 500) is an unmanaged group of securities considered to be representative of the stock market in general.

The Dow Jones Industrial Average is a price-weighted average of 30 significant stocks traded on the New York Stock Exchange and the NASDAQ.

The Nasdaq is a computerized system that facilitates trading and provides price quotations on some 5,000 of the more actively traded over-the-counter stock.

[1] http://briefing.com/investor/markets/weekly-wrap/weekly-wrap-for-july-29-2013.htm

[2] http://www.businessweek.com/articles/2013-07-31/gdp-growth-beats-expectations-remains-soft

[3] http://www.reuters.com/article/2013/08/02/us-usa-economy-idUSBRE96A0G320130802

[4] http://www.businessinsider.com/july-30-31-fomc-meeting-statement-2013-7

[5] http://www.reuters.com/article/2013/08/02/us-usa-fed-bullard-unemployment-idUSBRE97112A20130802